Unpacking the Business Owner's Policy: Essential Coverage for Your Small Business

November 15, 2025

Why Your Small Business Needs an Insurance Safety Net

A small business owners insurance policy is a crucial safety net, protecting your business from financial losses due to lawsuits, property damage, and unexpected events that could otherwise force you to close.

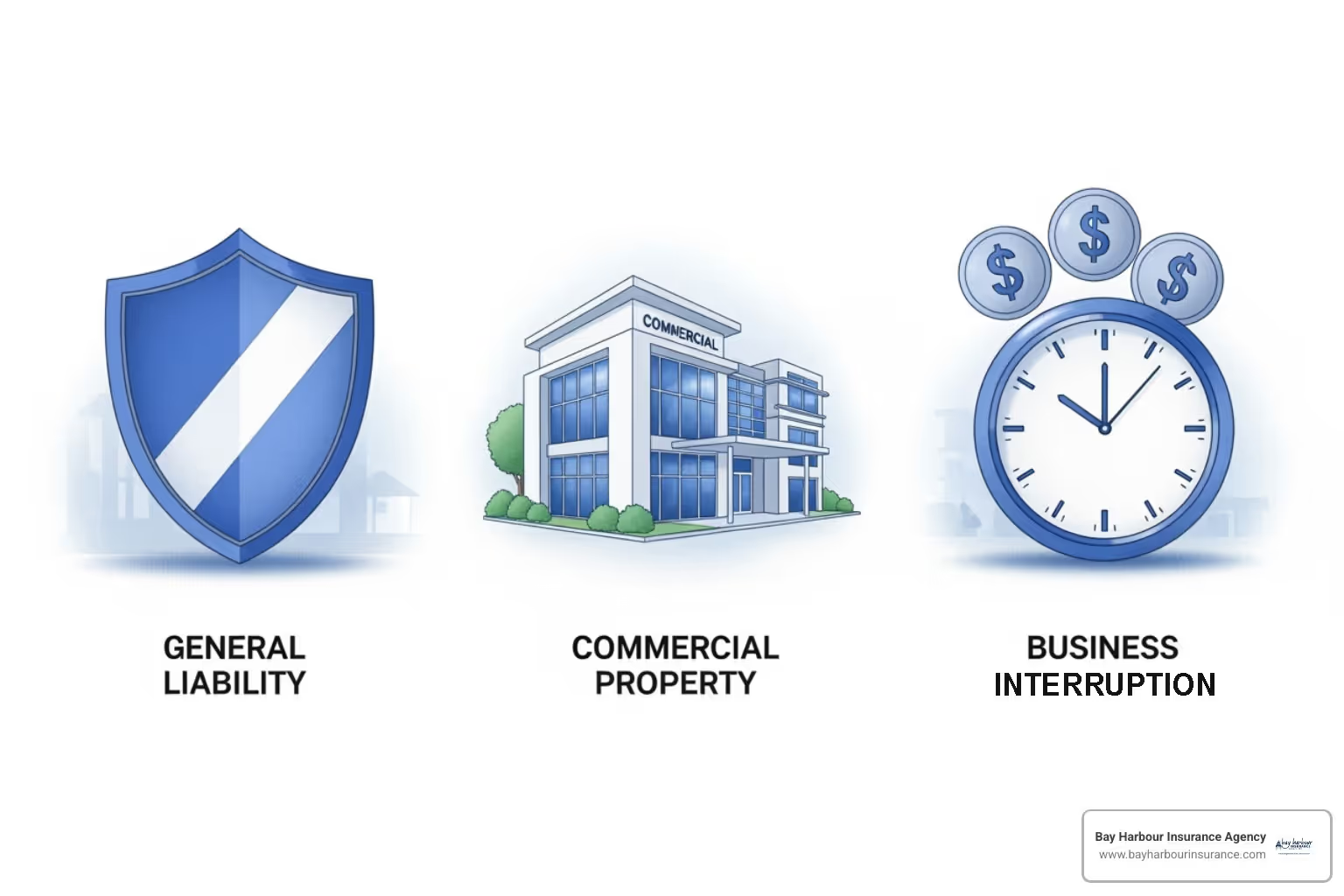

Key Components of Small Business Insurance:

- General Liability - Covers third-party injury claims and property damage

- Commercial Property - Protects your building, equipment, and inventory

- Business Interruption - Replaces lost income when you can't operate

- Professional Liability - Covers mistakes in services or advice

- Cyber Liability - Protects against data breaches and cyber attacks

You've invested your time and money into your Long Island business. But as one insurance broker noted: "I have dozens of examples of small businesses hit with lawsuits alleging negligence or faulty products. The entrepreneur ends up losing a fortune or even goes bankrupt."

The reality is stark: Statistics Canada data shows 700,000 civil court cases went to trial in 2020, with about half brought against small business owners. The average claim could cost your business tens of thousands of dollars.

Without proper protection, a single lawsuit or covered loss could wipe out your personal assets and everything you've worked to build. A comprehensive policy transfers these risks to an insurer for an affordable premium, giving you the peace of mind to focus on growth.

Decoding the Business Owner's Policy (BOP): Your All-in-One Solution

Juggling multiple insurance policies with different renewal dates and agents can be overwhelming. The Business Owner's Policy (BOP) simplifies this by bundling essential coverages into one package, often saving you money. This bundled coverage approach is designed for small to medium-sized businesses.

A BOP's value is its cost-effectiveness and convenience, offering comprehensive protection without the hassle of managing multiple policies. It's insurance made simple for busy business owners.

What General Liability Insurance Covers

General Liability Insurance is the foundation of your small business owners insurance policy and your first line of defense. If a customer slips in your Patchogue café or your crew damages a client's property in Holbrook, this coverage handles the fallout.

It covers third-party claims for bodily injury, property damage, and advertising injury (like copyright infringement). Crucially, it also pays for legal defense costs, which can be substantial even if you're not at fault. Without it, a single incident could lead to thousands in medical bills and legal fees.

What Commercial Property Insurance Covers

Your physical assets—the building in Sayville, equipment in your Medford workshop, or inventory in your Bellport boutique—are vital. Commercial Property Insurance protects these assets.

It covers your furniture, fixtures, computers, machinery, and other business personal property against perils like fire, theft, and vandalism. If a fire damaged your Holtsville office, this insurance provides the funds to replace everything from desks to servers, allowing you to recover without draining your savings.

What Business Interruption Insurance Covers

Property insurance may repair your building after a fire, but what about the income you lose while closed? Business Interruption Insurance is the financial lifeline that covers this gap.

It replaces lost income and helps pay for ongoing operating expenses like rent, utilities, and payroll when a covered event forces a temporary shutdown. Some policies also cover temporary relocation costs during the recovery period. This coverage ensures a covered peril doesn't turn a temporary setback into a permanent closure, allowing you to focus on rebuilding.

Customizing Your Small Business Owners Insurance Policy: Beyond the Basics

A Business Owner's Policy provides a solid foundation, but most businesses need to customize it. A Patchogue restaurant has different risks than a Sayville marketing consultant, so your small business owners insurance policy must be custom to your unique needs.

Customization means adding the right coverage, not just more coverage. We help you conduct a risk assessment to identify your specific vulnerabilities and build a policy around them.

Assessing Your Needs for a Small Business Owners Insurance Policy

Before customizing your policy, we must understand your business.

- Business size: BOPs are ideal for businesses with fewer than 50 employees and under $5 million in revenue. Larger companies may need a more complex commercial package policy.

- Location: A Long Island location means unique weather risks, especially in flood-prone areas. Local crime rates also factor in.

- Industry risks: A retail store's risks (theft, falls) differ from a contractor's (equipment damage, job site injuries) or a consultant's (faulty advice). We always ask: What single event could put you out of business?

- Annual revenue and number of employees: These factors help determine appropriate liability limits.

- Specific operations: Do you store valuable inventory, handle hazardous materials, or have clients visit your location? Each detail helps shape your coverage.

Common Endorsements and Additional Coverages

Once we understand your risks, we can add specialized coverages:

- Professional Liability Insurance (E&O): Essential if you provide advice or services (e.g., accountants, consultants). It covers claims that your professional errors cost a client money. Secure Your Business with Professional Liability Insurance.

- Cyber Liability Insurance: Crucial for any business that stores customer data or processes payments. The Risks of Not Having Cyber Insurance are significant in today's digital world.

- Commercial Auto Insurance: Necessary if your business owns vehicles or if employees use personal cars for work, as personal auto policies typically exclude business use.

- Workers' Compensation: Required by New York State law for businesses with employees. It covers medical costs and lost wages for on-the-job injuries and protects you from employee lawsuits.

- Directors & Officers Insurance: Protects the personal assets of company leaders if they are sued for management decisions. Learn the Directors & Officers Insurance Basics.

As an independent agency, we can mix and match these coverages to create the perfect small business owners insurance policy for you.

Home-Based Businesses: A Unique Small Business Owners Insurance Policy Challenge

Running a business from home creates unique insurance challenges. Your homeowner's policy is for your personal life and has significant limitations regarding business activities, leaving you financially vulnerable.

Most homeowner's policies exclude or provide very little coverage for business equipment, business-related liability claims (like a client falling in your home office), and lost business income. A standard policy's $2,500 limit for business equipment is rarely enough to replace computers, tools, or inventory.

To close these gaps, we recommend either a specific small business owners insurance policy for home-based businesses or adding business endorsements to your homeowner's policy, paired with separate liability coverage. These solutions are affordable and essential for protecting your home-based operation.

What Determines the Cost of Your Business Insurance?

Several factors determine the cost of your small business owners insurance policy. Understanding them can help you make smarter coverage decisions. Most premiums are also tax-deductible.

- Industry type: Higher-risk industries like construction pay more than lower-risk ones like graphic design.

- Business location: Insurers consider local crime rates, fire protection, and natural disaster risks like coastal flooding on Long Island.

- Business size and revenue: More employees and higher revenues mean greater potential for claims, increasing premiums.

- Claims history: A clean record keeps premiums down, while frequent claims signal higher risk and lead to higher costs.

- Property value and construction: A new building with sprinklers is cheaper to insure than an older one. The value of your equipment and inventory also affects the price.

- Coverage limits and deductibles: Higher coverage limits increase your premium, while higher deductibles can lower it.

- Risk management: Implementing safety training, cybersecurity measures, and maintenance programs can earn you discounts.

can influence annual premium ranges for business insurance, presented in a clear, easy-to-read format with calming blue and white colors and subtle textures. - small business owners insurance policy infographic brainstorm-6-items")

The cheapest small business owners insurance policy isn't always the best. The goal is to find the right coverage for your risks at a price that fits your budget. Working with an experienced agent helps you find the sweet spot between comprehensive protection and reasonable premiums.

Partnering for Protection: How to Choose and Manage Your Coverage

Choosing the right small business owners insurance policy is like finding a trusted business partner. At Bay Harbour Insurance Agency, we are Long Island business owners who understand the local challenges. Our client-centered approach means we offer personal service to protect your business.

The Value of an Independent Insurance Broker

As an independent agent, we aren't tied to one insurance company. We work with multiple top-rated insurers to shop for the best coverage at the right price for you. We assess your unique risks, tailor your policy to fit your needs, explain complex terms in plain English, and provide ongoing support long after the policy is in place. Whether you need help with a claim or have questions, we're here for you.\

Policy Review and Updating Your Coverage

Your business evolves, and your small business owners insurance policy should too. We recommend an annual review to ensure your coverage keeps pace with changes like hiring employees, expanding to a new location, buying new equipment, or offering new services.

During these reviews, we'll assess your operations, confirm your limits are appropriate, and ensure you understand the claims process. This proactive approach lets you focus on growth with confidence. For more insights, see 10 Reasons You Need an Insurance Agency Near You. For additional resources, Business Insurance Help can provide valuable information.

Frequently Asked Questions about Business Owner's Policies

We often hear the same thoughtful questions from small business owners across Long Island. It's natural to want clarity about your small business owners insurance policy when protecting everything you've built.

Let's walk through the most common concerns.

Is business insurance required by law in New York?

While a comprehensive small business owners insurance policy is a smart business decision, not all coverage is mandated by New York State. However, insurance is often required in these situations:

- Workers' Compensation: Required by law if you have any employees.

- Commercial auto insurance: Mandatory if your business owns vehicles.

- Lender requirements: Lenders will require property insurance to protect their investment in your business loan.

- Landlord requirements: Most commercial leases require you to carry General Liability and Commercial Property insurance.

- Regulatory requirements: Some professional licenses or associations mandate specific coverages.

In practice, most Long Island businesses need several types of coverage to operate legally and meet contractual obligations.

What is the difference between a BOP and a Commercial Package Policy (CPP)?

Both a Business Owner's Policy (BOP) and a Commercial Package Policy (CPP) bundle coverages, but they serve different needs.

- A BOP is a cost-effective, pre-packaged solution combining General Liability, Commercial Property, and Business Interruption. It's ideal for smaller businesses (fewer than 50 employees, under $5 million in revenue) with straightforward risks.

- A CPP is a flexible, custom-built solution for larger or more complex businesses with unique risks. It allows you to pick and choose from a wider array of coverages and tailor limits.

Most small businesses on Long Island are well-served by a BOP.

Can I get a BOP for my specific industry, like a restaurant or retail store?

Yes, BOPs are versatile and can be customized for many industries on Long Island.

- Restaurants can add endorsements for food spoilage or liquor liability. See our guide on Restaurant Insurance Coverage.

- Retail stores can get coverage for seasonal inventory changes or customer property.

- Professional services can add Professional Liability (E&O) to a BOP to cover claims related to their advice.

- Small contractors may also qualify for a BOP, though larger operations often need a CPP.

The key is to discuss your specific operations to see if a customized small business owners insurance policy is the right fit.

Conclusion: Secure Your Hard Work and Future Growth

You've poured your dedication into building your Long Island business. A single lawsuit, fire, or cyber attack could threaten all that hard work. A well-designed small business owners insurance policy is not just an expense; it's a shield that provides a financial safety net and peace of mind.

This proactive investment in your future allows you to take calculated risks and grow with confidence, knowing you're protected from the unexpected. At Bay Harbour Insurance Agency, our client-centered approach means we take the time to understand your unique goals and concerns. As an independent insurance agency in Long Island, we work for you, shopping multiple carriers to find the perfect fit.

We know Long Island because we are a Long Island business. We understand the local challenges and the personal touch that makes all the difference when you need support.

Don't leave your investment unprotected. Let us help you build an insurance strategy that protects your investment and secures your path to continued growth.

Ready to take the next step? Get a Business Insurance Quote on Long Island today, and let's start building your safety net together.