General Business (1+ employees)

New York Workers Compensation Insurance: Essential Guide for Employers

For businesses operating across Long Island—from the bustling Main Street of Patchogue to the industrial hubs in Medford— Workers’ Compensation Insurance isn’t just a legal requirement; it’s a vital safety net for your most important asset: your people. Every New York employer must understand workers compensation insurance.

Bay Harbour Insurance provides tailored coverage solutions for small to medium-sized businesses throughout Long Island and beyond. Whether you are running a medical facility near Horseblock Road in Medford, a retail shop in Holbrook, or a waterfront restaurant in Patchogue, our team ensures you meet New York State mandates while protecting your bottom line.

State law requires nearly all businesses with employees to maintain this coverage. The consequences of operating without proper workers compensation insurance can be severe—including criminal charges and substantial fines. This comprehensive guide walks you through New York state workers compensation requirements, coverage options, costs, and the steps to secure compliant protection for your workforce.

What is Workers Compensation Insurance and Why New York Requires It

Your business depends on good employees and their expertise, dedication, and hard work. In a fast-paced environment like the Sunrise Highway corridor or the busy intersections of Holtsville, accidents can happen in the blink of an eye. If an employee is injured in a work-related accident, Workers’ Compensation ensures they get the care they need so you can have peace of mind knowing everyone is properly protected.

Core Purpose of Workers Comp

Protects employees by guaranteeing medical treatment and partial wage replacement after a work injury or occupational illness

Shields employers from potentially devastating lawsuits related to workplace accidents

Creates a predictable system for handling workplace injury costs rather than uncertain litigation expenses

Establishes a state-regulated framework ensuring injured workers receive timely care and financial support

New York's Legal Mandate

New York law is strict, but your insurance experience should be personal. As a local agency based on Waverly Avenue in Patchogue, we understand the specific risks faced by our neighbors.

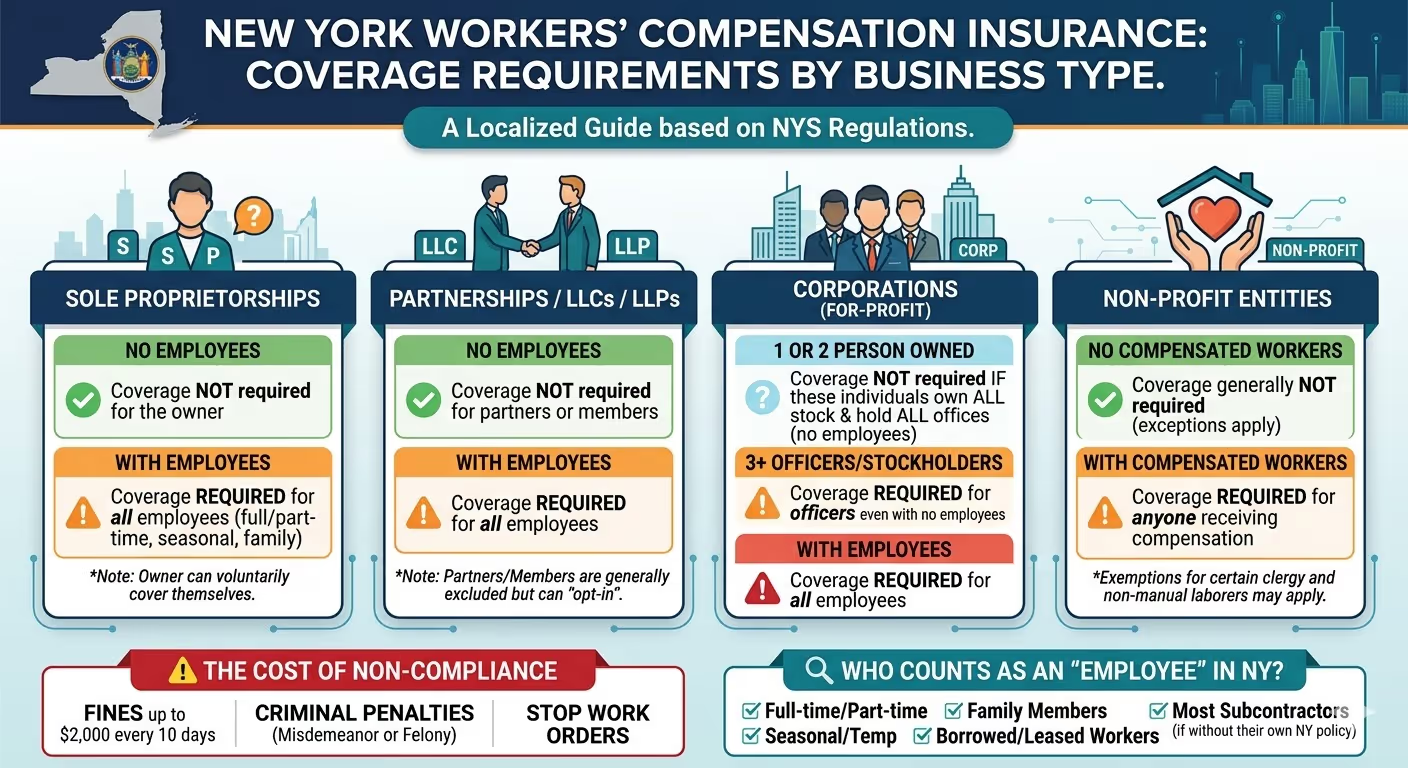

New York Workers Compensation Law requires virtually every employer to provide workers compensation insurance coverage. The law applies whether you have one employee or one thousand. Even part-time, seasonal, and temporary workers must be covered under most circumstances.

The New York Workers Compensation Board enforces these requirements. Failure to secure coverage results in serious penalties including fines up to $2,000 for every ten-day period without insurance, plus potential criminal charges.

Who Must Carry Workers Compensation Insurance in New York?

• Any business with one or more employees on payroll

• Construction industry employers (even with just one part-time worker)

• Employers of domestic workers who work 40+ hours per week

• Non-profit organizations with paid staff

• Government entities and public employers

Limited Exceptions: Sole proprietors with no employees, certain family farm operations, and some volunteer organizations may be exempt. However, even exempt businesses can purchase voluntary coverage.

Ensure Your Business Complies with NY Law

Don't risk penalties and legal action. Verify your workers compensation insurance requirements and get coverage quotes from licensed New York carriers today.

Get Free NY Workers Compensation Insurance QuoteNew York State Requirements for Workers Compensation Coverage

Understanding your specific obligations under New York state workers compensation law helps you maintain compliance and avoid costly penalties. Requirements vary based on business structure, industry, and workforce composition.

Coverage Requirements by Business Type

Business Type

Coverage Requirement

Key Details

Mandatory from first day of employment

Includes part-time, seasonal, and temporary workers. Coverage must be in place before the first employee begins work.

Construction Industry

Mandatory for all employers including sole proprietors with employees

Strict enforcement. Even one helper or subcontractor may trigger requirement. Must verify subcontractor coverage.

Sole Proprietor (no employees)

Not required but available

Can purchase voluntary coverage for self-protection. Some clients or contracts may require proof of coverage.

Partnership (no employees)

Not required for partners but mandatory for any employees

Partners can elect coverage. Once you hire anyone outside the partnership, coverage becomes mandatory.

Corporate Officers

Generally included but can file for exemption

Officers owning 10%+ of stock may exclude themselves by filing CE-200 form with the Workers Compensation Board.

Domestic Employees

Mandatory if working 40+ hours per week

Includes housekeepers, nannies, home health aides. Homeowners must secure domestic workers coverage.

Proof of Coverage Requirements

New York employers must display proof of workers compensation insurance at their workplace. You'll receive forms C-105.2 or DB-120.1 from your insurance carrier showing you have coverage. These notices must be posted in a visible location where employees can easily see them.

Additional Compliance Obligations

Maintain accurate payroll records for all employees (required for premium audits)

Report employee changes to your insurance carrier promptly

Classify workers correctly by industry class codes

File required forms with the New York Workers Compensation Board

Report serious workplace injuries within required timeframes

Cooperate with workplace safety inspections

Penalties for Non-Compliance

Operating without required workers compensation insurance in New York carries severe consequences:

• Civil penalties up to $2,000 for each 10-day period without coverage

• Criminal charges (misdemeanor) punishable by fines and potential jail time

• Stop-work orders immediately halting all business operations

• Personal liability for all costs of employee injuries during uninsured period

• Inability to bid on government contracts or construction projects

Verify Your Coverage Requirements

Unsure about your specific workers compensation obligations?

Get a free compliance review and discover exactly what coverage your New York business needs.

Speak with a compliance specialist: 631.758.1550

Types of Benefits Covered Under NY Workers Compensation

New York workers compensation insurance provides four main categories of benefits to employees who suffer work-related injuries or illnesses. Understanding these benefits helps employers appreciate the value this coverage delivers to their workforce.

Medical

Benefits

Full coverage for all necessary medical treatment related to the workplace injury or illness, with no deductibles or co-pays for the injured worker.

What's included: Emergency care, hospital stays, surgery, prescription medications, physical therapy, medical equipment, and ongoing treatment required for recovery.

Provider selection: For the first 30 days, the employer can direct medical care to specific providers. After 30 days, the injured employee can choose their own authorized medical provider from the workers comp network.

No time limit: Medical benefits continue for as long as treatment is medically necessary, even years after the initial injury.

Cash Benefits

(Wage Replacement)

Partial wage replacement when an injury prevents the employee from working or limits their earning capacity.

Temporary total disability: Pays two-thirds of the worker's average weekly wage (subject to state maximum) when completely unable to work during recovery.

Permanent partial disability: Compensates for permanent loss of function or earning capacity, calculated based on the injury severity and its impact on future earnings.

Temporary partial disability: Provides benefits when the worker can return to light duty at reduced wages during recovery.

Waiting period: Cash benefits typically begin after seven days of disability. If disability exceeds 14 days, benefits are retroactive to day one.

Death

Benefits

Financial support for dependents when a workplace injury or illness results in an employee's death.

Survivor benefits: Weekly payments to the deceased worker's spouse and dependent children, calculated based on the worker's average weekly wage and number of dependents.

Burial expenses: Up to a state-determined maximum for funeral and burial costs.

Duration: Benefits typically continue for the life of a surviving spouse (or until remarriage) and for dependent children until age 18 (or 23 if full-time students).

Important note: Death benefits ensure families maintain financial stability after losing a wage earner to a workplace tragedy.

Vocational Rehabilitation

When an injury prevents a worker from returning to their previous occupation, New York workers compensation may provide vocational rehabilitation services.

Job retraining programs to learn new skills

Career counseling and job placement assistance

Education and certification courses for new careers

Resume preparation and interview coaching

Maintenance allowances during retraining

Goal: Help injured workers return to gainful employment in a suitable occupation matched to their post-injury capabilities.

What Workers Compensation Does NOT Cover

• Pain and suffering damages (only economic losses are compensated)

• Punitive damages against the employer

• Injuries from employee intoxication or illegal drug use

• Injuries intentionally self-inflicted

• Injuries during voluntary recreational activities

• Injuries from fights or horseplay the employee instigated

• Injuries occurring during commute to/from work (with limited exceptions)

Important: In exchange for guaranteed benefits, employees generally cannot sue their employer for workplace injuries. This "exclusive remedy" provision protects employers from potentially unlimited lawsuit damages.

How to Obtain Workers Compensation Insurance in Long Island

New York employers have several options for securing required workers compensation coverage. The process varies slightly depending on which insurance route you choose, but all paths lead to the same goal—compliant protection for your workforce.

Coverage Options for New York Employers

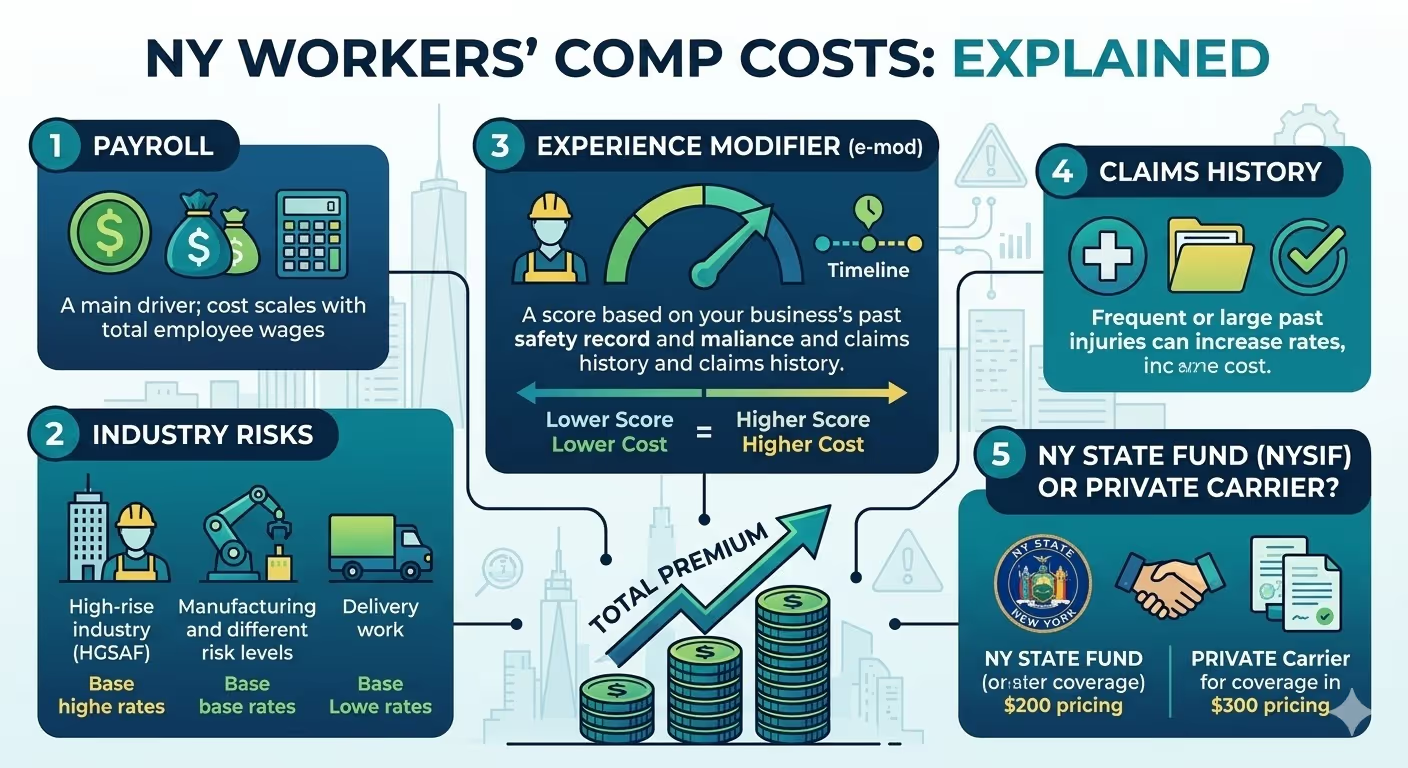

State Insurance Fund

The New York State Insurance Fund (NYSIF) operates as a self-supporting insurance carrier created by state law to ensure all employers can obtain coverage.

Advantages: Accepts all applicants regardless of claims history, competitive rates for many industries, extensive experience with New York-specific requirements.

Best for: New businesses, employers with poor loss history, high-risk industries, businesses unable to find private coverage.

Private Insurance Carriers

Dozens of licensed private insurance companies offer workers compensation insurance in New York, competing on price, service, and specialized industry expertise.

Advantages: Potential for lower premiums with good safety records, bundling options with other business insurance, personalized service, specialized programs for specific industries.

Best for: Established businesses with good safety records, employers seeking customized coverage, businesses wanting to bundle insurance policies.

Self-Insurance

Large, financially stable employers can apply to the Workers Compensation Board for permission to self-insure and pay claims directly rather than purchasing a policy.

Advantages: Potential cost savings for very large employers with strong safety programs, direct control over claims management, no insurance carrier overhead.

Best for: Major corporations with substantial financial resources, businesses with large, stable payrolls and excellent safety records.

Step-by-Step Process to Get Coverage

1Calculate Your Expected Payroll

Estimate your total annual payroll for all employees. Break down payroll by job classification since different occupations carry different risk levels and premium rates. Include regular wages, overtime, and certain bonuses in your calculation.

2 Determine Your Industry Classification Codes

Workers compensation premiums are based on classification codes assigned to different types of work. A code describes each job function at your business. Office workers carry different codes than construction laborers. Accurate classification is essential for proper pricing and compliance.

3 Request Quotes from Multiple Sources

Contact the New York State Insurance Fund and at least two or three private carriers to compare coverage options and pricing. Provide accurate payroll estimates and classification information to each carrier for comparable quotes.

4 Review Policy Terms and Costs

Compare not just premium costs but also payment plans, audit procedures, claims service quality, and any additional services like safety training or loss control assistance. The cheapest policy isn't always the best value.

5 Complete the Application

Provide detailed information about your business operations, payroll, ownership structure, prior workers comp claims history, and workplace safety programs. Accuracy is critical—misrepresentations can void coverage.

6 Submit Required Documentation

Carriers typically require your federal tax ID number, business formation documents, detailed payroll records, and loss history from previous carriers if applicable. Have these ready to speed the approval process.

7 Receive and Post Your Coverage Certificates

Once approved, you'll receive proof of coverage forms (C-105.2 or DB-120.1) that must be posted at your workplace. You'll also receive your policy documents detailing coverage terms, exclusions, and responsibilities.

8 Maintain Ongoing Compliance

Keep accurate payroll records throughout the policy term. Report any business changes to your carrier. Prepare for the end-of-year premium audit when your actual payroll is verified and final premium adjustments are made.

Required Information for Applications

Legal business name and DBA if applicable

Federal Employer Identification Number (FEIN)

Business structure (corporation, LLC, partnership, sole proprietor)

Complete description of business operations

Estimated annual payroll by job classification

Number of full-time, part-time, and seasonal employees

Prior workers comp claims history (last 5 years)

Current and prior insurance carrier information

Workplace locations and addresses

Safety programs and loss control measures in place

Common Application Mistakes to Avoid

• Underestimating payroll to reduce premiums (leads to large audit bills)

• Misclassifying employees into lower-rate codes (causes compliance issues)

• Failing to disclose prior claims or coverage gaps

• Not including all workers on the application

• Providing inaccurate business operation descriptions

• Missing application deadlines close to your start date

Tip: Work with an experienced insurance broker who specializes in New York workers compensation to avoid costly errors and find the best coverage options for your specific business.

Get Your Workers Compensation Coverage Today

Compare quotes from the New York State Insurance Fund and leading private carriers. Our specialists help you navigate the application process and secure compliant coverage quickly.

Get Free NY Workers Compensation Insurance QuoteCost of Workers Compensation Insurance in New York

Workers compensation insurance costs vary significantly based on your industry, payroll, claims history, and specific risk factors. New York employers typically pay between $0.75 and $15.00 per $100 of payroll, though high-risk industries can see rates exceeding $30 per $100 of payroll.

Key Factors That Determine Your Premium

Payroll Amount

Your total employee payroll is the foundation of workers comp pricing. Premiums are calculated per $100 of payroll. Higher total payroll means higher base premium, though large employers may qualify for volume discounts.

What counts: Regular wages, overtime pay, bonuses, vacation pay, sick pay, and certain other compensation.

Industry Classification Codes

Every job function receives a classification code with an assigned rate per $100 of payroll. Dangerous occupations like roofing or demolition carry much higher rates than clerical office work.

Example range: Office clerical workers might be $0.50 per $100 payroll while construction laborers could be $25 per $100 payroll.

Claims History

Your experience modification rate (mod) adjusts your premium based on past claims compared to similar businesses. A mod of 1.0 is average. Below 1.0 earns discounts; above 1.0 increases premiums.

Impact: A 0.75 mod saves 25% on premium. A 1.50 mod increases costs by 50%.

Business Location

New York rates vary slightly by region. Urban areas with higher wage levels and medical costs may see different pricing than rural regions, though differences are less significant than industry classification impacts.

Safety Programs

Documented safety training, workplace hazard controls, return-to-work programs, and strong safety cultures can qualify businesses for premium discounts with many carriers. Proactive risk management pays dividends.

Coverage Selection

While basic coverage is standardized, some optional features can affect cost—such as waiving your right to recover from negligent third parties, higher benefit limits, or voluntary coverage for otherwise exempt owners.

Sample Premium Calculations

Business Type

Annual Payroll

Rate per $100

Base Premium

Experience Mod

Final Premium

Small Retail Store (3 employees)

$120,000

$2.50

$3,000

1.00

$3,000

Restaurant (15 employees)

$450,000

$3.75

$16,875

1.15

$19,406

Office/Professional (8 employees)

$480,000

$0.85

$4,080

0.90

$3,672

Construction Company (25 employees)

$1,500,000

$18.50

$277,500

1.25

$346,875

Manufacturing (40 employees)

$2,200,000

$5.25

$115,500

0.85

$98,175

Note: These examples are illustrative. Actual rates depend on specific classification codes, carrier underwriting, loss history, and other factors. Contact carriers for precise quotes.

Strategies to Reduce Workers Compensation Costs

Implement comprehensive safety programs – Documented training, hazard assessments, and safety committees reduce injuries and demonstrate commitment to risk control.

Classify employees accurately – Ensure workers are in the correct, most specific classification codes. Don't overpay by using broader, higher-rated categories.

Manage claims proactively – Early injury reporting, modified duty programs, and active claims oversight minimize costs and improve your experience mod.

Maintain accurate payroll records – Proper record-keeping prevents overpayment during annual audits and supports proper classification.

Shop multiple carriers annually – Rates and underwriting appetite change. Compare New York State Insurance Fund with private carriers every renewal period.

Consider return-to-work programs – Getting injured employees back to modified duty quickly reduces indemnity costs and improves outcomes.

Review your experience mod – Understand which claims impact your mod most and dispute any errors in the calculation.

Pay premiums on time – Avoid late fees and maintain good carrier relationships that can lead to better terms.

Invest in workplace improvements – Ergonomic equipment, better lighting, non-slip surfaces, and proper tools prevent injuries before they happen.

Work with experienced brokers – Specialists in New York workers comp can find coverage options and cost-saving strategies you might miss on your own.

Understanding the Annual Premium Audit

Most workers compensation policies are initially priced on estimated payroll. At the end of your policy term, the insurance carrier audits your actual payroll to calculate the final premium.

• If actual payroll was higher than estimated, you owe additional premium

• If actual payroll was lower, you receive a partial refund

• Maintain detailed payroll records by employee and job classification

• The audit covers all compensation including overtime, bonuses, and other wages

• Cooperate fully with auditors to avoid delays or disputes

Tip: Don't dramatically underestimate payroll to lower your initial premium. You'll face a large bill at audit time, and it may indicate fraud to the carrier.

Calculate Your Workers Compensation Premium

Get an accurate cost estimate for your New York business.

Our specialists analyze your payroll, classifications, and claims history to find you the best rates.

Questions about your premium? 631.758.1550

Top Workers Compensation Insurance Providers in New York

New York employers can choose from the state-operated insurance fund and numerous private insurance carriers. Each offers different strengths in pricing, service, industry specialization, and claims management. Below are prominent options serving New York businesses.

Insurance Provider

Key Strengths

Target Businesses

Special Features

New York State Insurance Fund (NYSIF)

As the largest workers’ compensation carrier in New York, NYSIF’s primary strength is its "Guaranteed Issue" mandate—they must provide coverage to any New York employer, regardless of risk level or past loss history. Unlike private carriers that may "cherry-pick" low-risk industries, NYSIF provides a stable safety net for high-risk sectors. They are financially self-supporting and recently achieved a milestone of over 2 million same-day benefit payments, demonstrating a massive scale of operational efficiency.

NYSIF is the primary choice for High-Risk Industries (such as heavy construction, roofing, and trucking) that may struggle to find affordable coverage in the voluntary market. However, they have recently pivoted to target Small Businesses and Startups through a dedicated Office of Small Businesses. They are also a top choice for Diversity-Focused Firms, as they lead the state in MWBE (Minority and Women-owned Business Enterprise) utilization and recently introduced gender-neutral pricing for disability benefits, ensuring employers aren't penalized for the demographic makeup of their workforce.

Multi-State Coverage: Previously restricted to NY only, NYSIF now offers a program for NY-based employers to cover their employees in other states, eliminating the need for multiple

Safety Groups: They offer industry-specific "Safety Groups" which allow similar businesses to pool their risk and potentially earn significant year-end cash dividends (collectively returning $585 million to policyholders in a recent cycle).policies.

PayGo & Mobile Tech: Their "PayGo" real-time billing and a revamped Claim Mobile App provide modern, "insurtech" style convenience for both the employer and the injured worker.

Climate & Wellness Initiatives: Unique programs like the Climate Action Premium Program and specialized credits for Personal Protective Equipment (PPE) for extreme heat show a forward-thinking approach to modern workplace hazards.

Utica National Insurance Co

Founded in 1914 and headquartered in New York, Utica National is a "Super Regional" carrier with deep roots in the Empire State. Their primary strength lies in their financial stability (A.M. Best "A" rating) and their long-standing commitment to the independent agency model, ensuring personalized service. They are particularly noted for their "Uti-CARE" program, which focuses on quality medical case management to get employees back to work faster while controlling costs for the employer.

Utica National has a broad appetite but excels in serving Artisan Contractors, Auto Services/Repair shops, Child Care Centers, and Educational Institutions. They are an ideal fit for established mid-sized New York businesses looking for a carrier with a local presence and a specialized focus on safety and risk management.

Their "Right Pay" pay-as-you-go billing option is a major draw for New York businesses looking to manage cash flow by aligning premium payments with actual payroll cycles. Additionally, they offer a Direct Deposit option for claimant payments, which streamlines the benefits process for injured workers.

AmTrust / Wesco Insurance Co.

AmTrust (often writing through its subsidiary, Wesco Insurance Co.) is the #3 workers' compensation provider in the U.S. and a powerhouse in the New York market. Their strength lies in their massive "appetite" for diverse industries—covering over 350 class codes—and their industry-leading technology. They are frequently recognized for their superior claims handling, with adjusters managing lower-than-average caseloads to ensure more attentive service.

AmTrust is the "go-to" for Small to Mid-Sized Enterprises (SMEs). They specialize in Retail stores, Restaurants, Professional Offices (Doctors/Dentists), and Private Schools. Because they are comfortable with a wide variety of "low-risk preferred" classes, they are often the most competitive option for standard main-street businesses.

They offer the proprietary Pay-As-You-Owe® (PAYO®) system, which integrates directly with many payroll providers to eliminate down payments and simplify the year-end audit process. Their Loss Control Department provides policyholders with free access to an extensive library of online safety training and streaming videos specifically designed to reduce workplace hazards in high-turnover industries like hospitality.

How to Choose the Right Carrier for Your Business

Evaluate financial strength: Check carrier ratings from AM Best, Moody's, or Standard & Poor's to ensure they can pay claims.

Compare total cost: Look beyond the premium—consider payment plans, deposit requirements, and audit processes.

Assess claims service: Research carrier reputation for claims handling speed, fairness, and injured worker satisfaction.

Review safety resources: Determine what loss control services, training materials, and risk management support each carrier provides.

Consider industry expertise: Some carriers specialize in your industry and understand your specific risks better than generalists.

Check service accessibility: Evaluate online tools, local claims offices, and availability of dedicated representatives.

Compare Quotes from Multiple New York Carriers

Don't settle for the first quote. Our insurance specialists help you compare coverage options from NYSIF and leading private carriers to find the best protection at the most competitive price.

Get Free NY Workers Compensation Insurance QuoteOr call to speak with a New York workers comp specialist 631.758.1550

How to File a Workers Compensation Claim in New York

When a workplace injury occurs, following the correct claim process protects both the injured employee and the employer. New York has specific procedures and deadlines that must be met to ensure proper handling of workers compensation claims.

Step-by-Step Claim Filing Process

1 Immediate Response to Workplace Injury

When an employee is injured, ensure they receive necessary medical attention immediately. Life-threatening emergencies require calling 911. For non-emergency injuries, direct the worker to an authorized medical provider within your workers comp network for the first 30 days of treatment.

Document everything: Note the time, location, witnesses, and circumstances of the injury. Take photos of the accident scene and any equipment involved if possible.

2 Employee Reports Injury to Employer

The injured worker must notify their employer of the injury as soon as possible. While New York allows up to 30 days for written notice, immediate reporting ensures faster claims processing and medical treatment authorization.

Employer responsibility: Provide Form C-2F (Employer's Report of Work-Related Injury/Illness) to the employee to complete. Do not discourage injury reporting—this is illegal and can result in penalties.

3 Employer Files Required Forms

Employers must file Form C-2 (Employer's Report) with their insurance carrier and the Workers Compensation Board within 10 days of learning about the injury. Include all requested information about the employee, injury details, and circumstances.

Electronic filing: Most carriers accept and prefer electronic submission. The Workers Compensation Board also offers online filing through their portal.

4 Insurance Carrier Begins Investigation

The insurance carrier reviews the claim, investigates the circumstances, and determines whether the injury is compensable under workers compensation law. This process typically takes several days to a few weeks.

Cooperation required: Employers should provide requested documentation, witness statements, and any additional information the carrier needs.

5 Medical Treatment Commences

The injured employee receives treatment from authorized medical providers. For the first 30 days, the employer can direct care to specific providers. After 30 days, the employee may choose from authorized providers in the network.

No cost to employee: All approved medical treatment is fully covered with no deductibles or co-payments required from the injured worker.

6 Carrier Authorizes or Denies Claim

The insurance carrier either accepts the claim and begins benefit payments or denies the claim if they determine the injury is not work-related or not covered. Denials must be in writing with specific reasons.

If denied: The employee can request a hearing before a Workers Compensation Law Judge to contest the denial.

7 Wage Replacement Benefits Begin (If Applicable)

If the injury causes the worker to miss more than seven days of work, cash benefits begin. Benefits are retroactive to day one if disability exceeds 14 days. Payments are typically two-thirds of the worker's average weekly wage, subject to state maximum limits.

8 Ongoing Claims Management

The insurance carrier manages the claim throughout treatment and recovery. This includes coordinating medical care, authorizing treatment, paying benefits, and monitoring the employee's progress toward returning to work.

Stay involved: Employers should maintain contact with injured workers, offer modified duty when possible, and work with the carrier on return-to-work planning.

Required Forms and Deadlines

Form

Who Files

Deadline

C-2F (Employee Statement)

Injured Employee

Within 30 days of injury (sooner is better)

C-2 (Employer Report)

Employer

Within 10 days of learning of injury

C-3 (First Report of Injury)

Insurance Carrier

Within 18 days of receiving employer's report

C-4 (Claim for Benefits)

Employee (for cash benefits)

Within 2 years of injury or disability

Real-World Claim Examples

Long Island Restaurant Server - Slip and Fall

Incident: A server slipped on a wet kitchen floor during a busy dinner service and fractured her wrist.

Response: Manager documented the incident immediately, ensured medical care at an authorized urgent care clinic, and filed Form C-2 within 48 hours.

9 Medical benefits: Emergency care, orthopedic consultation, surgery, physical therapy—all fully covered

10 Lost wages: Unable to work for 8 weeks; received two-thirds of her average weekly wage during recovery

11 Return to work: Started modified duty (hostess role, no carrying) during final recovery phase

Outcome: Total claim cost approximately $42,000. Employee made full recovery and returned to regular duties. Employer's experience mod increased slightly but strong safety improvements prevented future increases.

Patchogue Construction Worker - Equipment Injury

Incident: A carpenter suffered a severe hand injury when a power saw malfunctioned at a residential construction site.

Response: Co-workers called 911 immediately. Employer reported injury to carrier same day and began immediate safety investigation of equipment.

12 Medical benefits: Emergency surgery, multiple follow-up procedures, ongoing therapy, specialized equipment

13 Lost wages: Permanent partial disability—unable to return to carpentry but retrained for estimating role

14 Vocational rehab: Six-month training program for construction estimating and project management

Outcome: Total claim cost exceeded $280,000 including medical care, cash benefits, and vocational training. Worker successfully transitioned to new career. Employer implemented enhanced equipment safety protocols.

Common Claim Filing Mistakes to Avoid

15 Delayed reporting: Late injury reports complicate investigations and can result in denied claims

16 Incomplete documentation: Missing details about injury circumstances make claims processing difficult

17 Discouraging employees from filing: Illegal and can result in penalties plus additional liability exposure

18 Failing to offer modified duty: Keeps employees out of work longer and increases claim costs

19 Poor communication with carrier: Delays claims resolution and prevents effective case management

20 Not investigating root causes: Missing opportunities to prevent similar future injuries

Need Help Managing Workers Comp Claims?

Effective claims management reduces costs and helps injured employees recover faster.

Get expert guidance on claim procedures, return-to-work programs, and loss control strategies.

Employer Responsibilities and Penalties for Non-Compliance

New York takes workers compensation compliance seriously. Employers must understand their legal obligations and the severe consequences of failing to maintain required coverage. This section outlines key responsibilities and enforcement actions.

Core Employer Obligations Under New York Law

Insurance Coverage Requirements

21Obtain and maintain workers compensation insurance from day one of having employees

22Ensure coverage remains active without any gaps or lapses

23Purchase adequate coverage limits to protect all employees fully

24Notify your carrier immediately of business changes affecting coverage

25Pay all premiums on time to prevent policy cancellation

26Cooperate with annual payroll audits and provide accurate records

Workplace Posting and Notice

27Display Form C-105.2 or DB-120.1 (proof of coverage) prominently where employees can see it

28Post notices in English and any other languages commonly spoken by your workforce

29Update posted notices whenever you change insurance carriers

30Provide new employees with information about workers comp rights and procedures

Injury Reporting and Claims

31File Form C-2 (Employer's Report) within 10 days of learning about any workplace injury

32Provide injured workers with Form C-2F to complete their portion

33Report all injuries to your insurance carrier promptly

34Cooperate fully with carrier investigations and provide requested information

35Never discourage or prevent employees from reporting injuries or filing claims

36Maintain confidential medical information in compliance with privacy laws

Record Keeping

37Keep detailed payroll records for all employees by job classification

38Maintain documentation of all workplace injuries and illnesses

39Preserve safety training records and incident reports

40Retain workers comp policy documents and claims files for required periods

41Provide records to insurance auditors and Board investigators upon request

Penalties for Non-Compliance

Operating without required workers compensation insurance in New York carries some of the most severe penalties of any business regulation. The state aggressively enforces compliance through multiple mechanisms.

Civil Monetary Penalties

The Workers Compensation Board assesses penalties up to $2,000 for each 10-day period your business operates without required coverage.

Calculation example: 90 days without coverage = 9 ten-day periods × $2,000 = $18,000 in penalties, in addition to having to obtain coverage retroactively.

These penalties are in addition to any costs of injuries that occur during the uninsured period.

Criminal Charges

Failure to secure workers compensation coverage is a misdemeanor crime in New York, punishable by fines and imprisonment.

Potential sentences: Up to one year in jail, criminal fines, and a permanent criminal record that affects business licensing, bonding, and credibility.

Corporate officers can be held personally liable even in incorporated businesses.

Stop-Work Orders

The Workers Compensation Board can issue immediate stop-work orders forcing complete cessation of all business operations until coverage is obtained.

Impact: No revenue during shutdown, disrupted client relationships, employee layoffs, potential loss of contracts and business opportunities.

Orders remain in effect until proof of coverage and payment of all penalties.

Additional Consequences of Non-Compliance

42Personal liability for injuries: Without insurance, you are personally responsible for all medical costs and lost wages of injured employees—potentially hundreds of thousands of dollars

43Lawsuits: Injured employees can sue for damages when no workers comp coverage exists, exposing you to unlimited liability

44Inability to bid contracts: Most commercial clients and all government contracts require proof of workers compensation insurance

45License revocation: Professional and business licenses can be suspended or revoked for non-compliance

46Difficulty obtaining coverage: Gaps in coverage make it harder and more expensive to get insurance in the future

47Reputation damage: Criminal charges and stop-work orders become public record, harming business credibility

Enforcement Mechanisms

New York uses multiple methods to identify and penalize employers operating without workers compensation insurance:

48Random audits: The Board conducts surprise compliance checks across industries

49Employee complaints: Workers can report employers lacking coverage anonymously

50Injury investigations: Every reported workplace injury triggers a coverage verification

51Tax records cross-checking: State payroll tax filings are matched against insurance records

52Industry sweeps: High-risk industries face coordinated compliance enforcement campaigns

53Construction site inspections: Active construction sites are regularly checked for proper coverage

What to Do If You Receive a Penalty Notice

1 Obtain Coverage Immediately

Contact the New York State Insurance Fund or a private carrier to secure coverage right away. Most can bind coverage within 24-48 hours for standard risks.

2 Respond to All Official Notices

Do not ignore letters from the Workers Compensation Board. Respond by the deadline and provide all requested documentation.

3 Request a Hearing if Appropriate

You have the right to contest penalties if you believe they are incorrect. Request a hearing before a Board administrative law judge.

4 Consider Legal Representation

Workers compensation attorneys can help navigate penalty proceedings, negotiate settlements, and protect your rights during enforcement actions.

5 Demonstrate Good Faith Compliance

Show the Board you are taking immediate corrective action. Maintain continuous coverage going forward and implement strong compliance procedures.

Avoid Penalties—Get Compliant Coverage Now

Don't wait for a penalty notice or stop-work order.

Secure your required workers compensation insurance today and protect your business from devastating enforcement actions.

Urgent compliance questions: 631.758.1550

Tips for Businesses to Manage Workers Compensation Costs

While workers compensation insurance is mandatory, New York businesses can take proactive steps to control costs while maintaining full compliance. Effective cost management focuses on injury prevention, smart claims handling, and strategic insurance purchasing.

Injury Prevention Strategies

The most effective way to reduce workers compensation costs is preventing injuries before they happen. Every dollar invested in safety typically saves three to six dollars in claims costs.

Comprehensive Safety

Programs

54Conduct regular workplace hazard assessments

55Implement written safety policies and procedures

56Provide job-specific safety training for all employees

57Establish a safety committee with worker participation

58Conduct routine safety inspections and correct hazards promptly

59Track near-miss incidents to prevent future injuries

Proper Equipment and

Ergonomics

60Invest in ergonomic workstations and tools

61Provide appropriate personal protective equipment

62Maintain equipment in safe working condition

63Replace worn or damaged safety equipment immediately

64Design workflows to minimize repetitive strain and overexertion

65Ensure adequate lighting and proper ventilation

Employee Training and

Engagement

66Provide thorough safety orientation for new hires

67Conduct ongoing refresher training regularly

68Train employees to identify and report hazards

69Reward safe behaviors and safety suggestions

70Encourage open communication about safety concerns

71Hold supervisors accountable for safety oversight

Effective Claims Management

How you handle claims after injuries occur significantly impacts your total costs and future premiums. Proactive claims management reduces both direct costs and your experience modification rate.

Immediate Response

Protocols

72Report quickly: File claims with your carrier within 24 hours of learning about injuries

73Document thoroughly: Gather witness statements, photos, and detailed incident reports immediately

74Provide medical care: Direct employees to authorized providers promptly to start treatment

75Show concern: Contact injured employees regularly to demonstrate genuine care for their recovery

76Investigate causes: Determine root causes of incidents to prevent recurrence

Return-to-Work

Programs

77Offer modified duty: Create temporary light-duty positions matching medical restrictions

78Stay connected: Maintain contact with injured workers throughout recovery

79Coordinate with providers: Work with treating physicians to facilitate safe return to work

80Be flexible: Adjust schedules and duties to accommodate recovering employees

81Track progress: Monitor transitional duty arrangements and adjust as recovery progresses

Benefits of Strong Return-to-Work Programs

82Reduces total claim costs by 30-50% on average

83Keeps valuable employees engaged with your business

84Maintains productivity during recovery periods

85Speeds overall recovery through purposeful activity

86Demonstrates compliance with disability accommodation laws

87Improves your experience modification rate

88Builds employee loyalty and morale

Strategic Long Island Insurance Purchasing

Smart insurance buying practices help you secure the best coverage at the most competitive rates available for your risk profile.

Shop Multiple Carriers

Compare quotes from NYSIF and at least three private carriers annually. Rates and underwriting appetites change, and loyalty doesn't always pay in insurance.

Use an independent insurance broker who represents multiple carriers to streamline comparison shopping.

Classify Employees Accurately

Ensure workers are assigned to the most specific, accurate classification codes. Overly broad classifications often carry higher rates.

Review classifications with your agent annually as job duties evolve. Proper classification prevents overpayment without misrepresenting your operations.

Manage Your Experience Mod

Understand how your experience modification rate is calculated. Focus claims management on injuries that most impact the mod—typically mid-sized claims.

Review your mod worksheet annually for errors and request corrections if you find inaccuracies in the data.

Consider Payment Plans

Many carriers offer pay-as-you-go programs that base premiums on actual current payroll rather than estimates, smoothing cash flow and eliminating large audit bills.

Evaluate whether monthly payments or quarterly installments work better for your business cash flow.

Maintain Continuous Coverage

Gaps in coverage make you uninsurable with many preferred carriers and trigger penalties. Even brief lapses can result in higher rates for years.

Set renewal reminders 60-90 days before expiration to allow adequate time for shopping and binding new coverage.

Invest in Safety for Discounts

Many carriers offer premium discounts for documented safety programs, drug-free workplace policies, and participation in safety groups.

Ask your agent about available discounts and the specific requirements to qualify for each program.

Payroll and Audit Management

89Estimate payroll accurately: Provide realistic payroll projections when obtaining quotes to avoid large audit adjustments

90Track payroll by classification: Maintain detailed records showing which employees work in which job classifications

91Exclude eligible items: Understand which payroll components can be excluded (some employer contributions, certain expense reimbursements)

92Prepare for audits: Have organized payroll records, tax forms, and classification documentation ready when auditors visit

93Review audit results: Check premium audit calculations for accuracy and dispute any errors promptly

94Adjust estimates mid-term: If your payroll changes significantly during the policy period, notify your carrier to adjust premiums and avoid surprises

Common Claim Filing Mistakes to Avoid

95 Failing to separate payroll by proper job classifications

96 Including eligible overtime premiums in auditable payroll

97 Misclassifying owners or officers

98 Not documenting payroll exclusions properly

99 Underestimating seasonal or variable payroll

100 Poor record-keeping making verification difficult

Tip: Work with your accountant or payroll service to ensure workers comp audits align with your actual payroll data and classifications.

Long-Term Cost Reduction Metrics

Track these key performance indicators to measure the effectiveness of your cost management efforts:

Metric

What It Measures

Target Goal

Incident Rate

Number of recordable injuries per 100 full-time workers per year

Below industry average for your classification

Experience Modification Rate

Your claims history compared to similar businesses (1.0 = average)

Below 1.0 (credit mod) and trending downward

Average Claim Cost

Total dollars paid per claim

Decreasing year over year through claims management

Lost Time Days

Days of work missed due to injuries

Minimized through return-to-work programs

Premium as % of Payroll

Workers comp cost as percentage of total payroll

At or below industry benchmarks for your class codes

Reduce Your Workers Compensation Costs

Get a comprehensive cost analysis and customized recommendations to lower your workers compensation expenses while improving workplace safety and claims outcomes.

Protect Your Business and Employees with Proper Workers Compensation Coverage

New York workers compensation insurance is not optional—it's a legal requirement that protects both your employees and your business. Understanding your obligations, securing appropriate coverage, and implementing strong safety and claims management practices positions your business for compliance and cost control.

Take action today to verify your coverage meets New York state requirements. Review your current policy limits, compare carrier options annually, and invest in injury prevention programs that reduce both human suffering and financial costs. Compliance protects you from severe penalties while proper coverage ensures your employees receive care when workplace injuries occur.

Get Your New York Workers Compensation Quote Today

Compare coverage from NYSIF and top-rated private carriers.

Our specialists help you secure compliant protection at competitive rates while navigating New York's complex requirements.

Speak with a New York workers comp expert: 631.758.1550

Frequently Asked Questions About New York Workers Compensation Insurance

Who is required to have workers compensation insurance in New York?

Nearly every New York employer must carry workers compensation insurance. If you have even one employee on payroll, you are generally required to provide coverage. This includes part-time, seasonal, and temporary workers. The construction industry has particularly strict requirements—even sole proprietors with a single helper need coverage. Limited exceptions exist for some sole proprietors with no employees, certain family farm operations, and specific volunteer organizations, but most businesses must maintain continuous coverage.

101Verify your requirements with the New York Workers Compensation Board or consult an insurance professional specializing in New York coverage.

What happens if I don't have workers compensation insurance in New York?

Operating without required workers compensation insurance in New York results in severe penalties. The Workers Compensation Board can assess civil fines up to $2,000 for every 10-day period you operate without coverage. Failure to secure coverage is also a criminal misdemeanor punishable by fines and up to one year in jail. The Board can issue stop-work orders immediately halting all business operations. Additionally, you become personally liable for all medical costs and lost wages of any employee injured during the uninsured period, potentially hundreds of thousands of dollars.

102If you are currently operating without coverage, obtain insurance immediately through the New York State Insurance Fund or a private carrier to avoid these serious consequences.

How much does workers compensation insurance cost in New York?

Workers compensation insurance costs vary widely based on your industry, payroll, and claims history. New York employers typically pay between $0.75 and $15.00 per $100 of payroll for most industries, though high-risk occupations like roofing or demolition can exceed $30 per $100 of payroll. A small office with $200,000 in annual payroll might pay $1,500-$3,000 annually, while a construction company with the same payroll could pay $30,000-$50,000 or more. Your experience modification rate, which reflects your claims history, also significantly impacts your final premium.

103Request quotes from multiple carriers including the New York State Insurance Fund to find the most competitive rate for your specific business.

What benefits does workers compensation provide to injured employees in New York?

New York workers compensation insurance provides comprehensive benefits to employees suffering work-related injuries or illnesses. Medical benefits cover all necessary treatment with no deductibles or co-pays for the injured worker. Cash benefits replace approximately two-thirds of the employee's average weekly wage when they cannot work due to the injury. Death benefits provide financial support to dependents if a workplace injury proves fatal. Vocational rehabilitation helps injured workers retrain for new careers when they cannot return to their previous occupation. All these benefits are provided regardless of who caused the accident.

104Employees should report workplace injuries immediately to ensure they receive all entitled benefits without delay.

Can I buy workers compensation insurance from any carrier?

You must purchase workers compensation insurance from a carrier licensed to sell coverage in New York. Options include the New York State Insurance Fund (which must accept all applicants) and numerous private insurance carriers authorized by the state. Not all carriers write coverage for all industries or accept all applicants. Businesses with poor claims history or high-risk operations may find their options limited to NYSIF or specialized carriers. Large, financially stable employers may also apply to self-insure with approval from the Workers Compensation Board.

105Work with an independent insurance broker who represents multiple carriers to find the best coverage options and pricing for your specific business needs.

How do I file a workers compensation claim in New York?

When a workplace injury occurs, the employee should report it to their employer immediately. The employer must then file Form C-2 (Employer's Report) with their insurance carrier and the Workers Compensation Board within 10 days. The injured employee completes Form C-2F and may need to file Form C-4 to claim cash benefits. The insurance carrier investigates the claim and either accepts it and begins paying benefits or denies it with written explanation. All necessary medical treatment should begin immediately through authorized providers in the workers comp network.

106Early reporting and proper documentation significantly improve claims processing speed and outcomes for both employees and employers.

Do I need workers compensation insurance for independent contractors?

True independent contractors are generally not covered under your workers compensation policy and are responsible for their own coverage. However, New York law and the Workers Compensation Board scrutinize independent contractor relationships carefully. If the Board determines your "contractors" are actually employees based on control factors, you can be held liable for coverage. In construction, you must verify that all subcontractors carry their own valid workers compensation insurance and obtain certificates of insurance. Misclassifying employees as independent contractors to avoid workers comp costs is illegal and results in severe penalties plus retroactive coverage obligations.

107Consult with legal and insurance professionals to properly classify workers and ensure compliance with New York's strict independent contractor rules.

Can business owners and corporate officers get workers compensation coverage?

Yes, but requirements vary by business structure. Sole proprietors and partners without employees are not required to carry coverage but can purchase voluntary workers compensation insurance for themselves. Corporate officers are generally included in coverage automatically, but officers owning 10% or more of corporate stock can file Form CE-200 to exclude themselves from coverage. Many business owners choose to maintain coverage even when exempt because it protects their personal finances if they're injured while working, and some clients or lenders require proof of coverage for all business principals.

108Discuss your specific situation with your insurance carrier or broker to determine the best approach for owner coverage in your business structure.

What is an experience modification rate and how does it affect my premium?

Your experience modification rate (mod or EMR) is a multiplier that adjusts your workers compensation premium based on your claims history compared to similar businesses. A mod of 1.00 is average—meaning your claims experience matches expectations for your industry. A mod below 1.00 (such as 0.80) means you have fewer or less severe claims than average and earns you a 20% discount. A mod above 1.00 (such as 1.30) indicates worse-than-average claims history and increases your premium by 30%. Your mod is calculated using three years of claims data and updated annually.

109Focus on injury prevention and effective claims management to improve your experience mod and reduce long-term workers compensation costs.

Additional questions about New York workers compensation insurance?

Contact a licensed insurance specialist at 631.758.1550 or