Insuring Your Future: A Guide to Top Company Insurers

October 31, 2025

Why Understanding Company Insurers Matters for Your Financial Security

Company insurers are the financial institutions that provide protection against life's unexpected events by pooling risk across thousands of policyholders. When you pay premiums to an insurance company, you're joining a large group where everyone contributes to a fund that pays out claims when members experience covered losses.

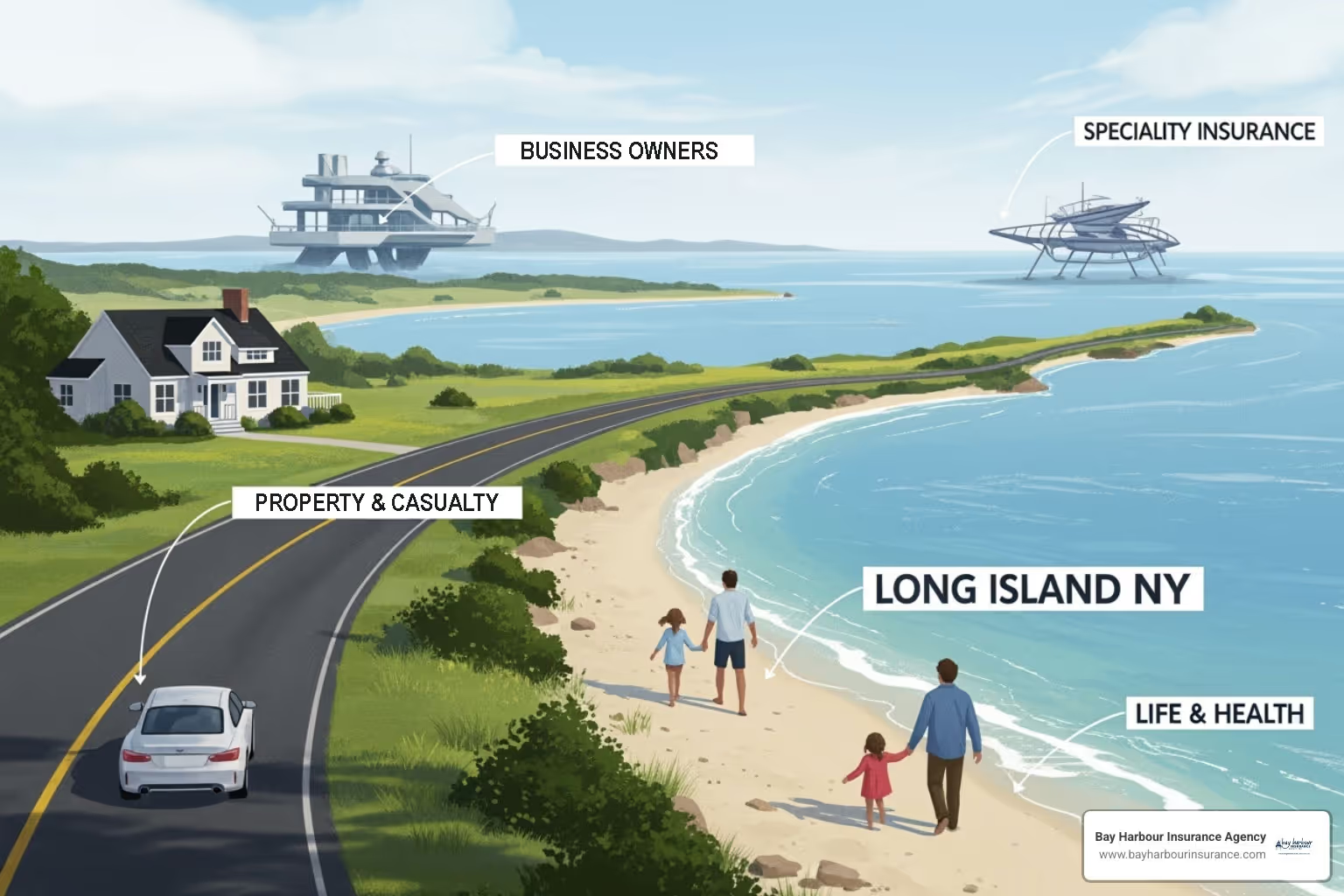

Top types of company insurers include:

- Property & Casualty Insurers - Cover homes, cars, and liability.

- Life & Health Insurers - Provide life insurance and health coverage.

- Supplemental Insurers - Fill gaps in traditional coverage.

- Specialty Insurers - Focus on specific risks or industries.

Key factors when choosing insurers:

- Financial Strength Ratings - A+ ratings from A.M. Best indicate superior financial stability.

- Claims Service - How quickly and fairly they handle your claims.

- Coverage Options - Whether they offer the specific protection you need.

- Customer Service - 24/7 support and easy policy management.

The insurance industry has evolved with technology, offering everything from mobile apps for policy management to AI-powered risk assessment. Many top insurers now provide 24/7 customer support and mobile ID cards, while others focus on specialized coverage for emerging risks.

For Long Island residents and business owners, understanding these different types of insurers helps you make informed decisions about protecting your home, car, or business. The right insurer should offer both financial stability and personalized service to meet your unique needs.

The Mechanics of Insurance: How Providers Assess Risk and Set Premiums

Ever wonder how company insurers determine your premium? Behind every quote is a careful process of underwriting that combines math, data, and experience to predict risk.

Underwriters act as financial detectives, piecing together your risk profile. When you apply for insurance, they analyze factors like your driving record or property location to answer one key question: "What is the likelihood this person will file a claim?" For auto insurance, an underwriter examines your driving history, car type, and commute distance. A driver with a clean record who garages their car will likely pay less than one with speeding tickets who parks on a busy street. It's not personalit's just math.

This risk assessment relies on actuarial science. Actuaries analyze historical data to spot patterns and predict future losses. They use the Law of Large Numbers, which states that with more data, predictions become more accurate. By pooling thousands of similar risks, company insurers can accurately estimate how much money they'll need for claims.

Factors you might not expect can also affect your rates. Your credit score, for instance, has been shown to correlate with claim frequency, a connection backed by solid data. You can learn more about Credit Score and Insurance Premiums and how they connect.

Technology is also changing the game. Telematics devices can monitor your actual driving habits, not just your past record. Safe drivers can benefit from this usage-based insurance technology and potentially Usage-Based Insurance: Save Money on their premiums.

The goal is to make insurance fair. Company insurers must collect enough in premiums to pay claims, cover costs, and remain financially strong. This careful data analysis ensures that insurance is both affordable and reliable when you need it most.

A Look at Different Types of Company Insurers

The insurance world is diverse, with different company insurers specializing in protecting specific aspects of your life and business. Understanding these distinctions helps you find the right coverage for your unique needs.

Property & Casualty (P&C) insurers are likely the most familiar. These are the company insurers that protect your home, car, and shield you from liability. When a tree falls on your roof or you're in a car accident, P&C insurers step in to help cover the costs.

Life & Health insurers focus on your family's well-being. Life insurance provides financial security for your loved ones, while health coverage helps manage medical costs.

Supplemental insurers fill gaps left by traditional health plans, often paying cash benefits directly to you to cover out-of-pocket expenses.

Specialty insurers tackle unique risks that don't fit into other categories, such as cyber insurance for businesses or professional liability for specific occupations.

Understanding the Models of Company Insurers

Beyond what they cover, company insurers operate under different business models.

FeatureStock InsurersMutual InsurersOwnershipOwned by shareholdersOwned by policyholdersPrimary FocusGenerate profits for investorsProvide value to policyholdersProfit DistributionDividends to shareholdersOften returned as policyholder dividendsDecision MakingBoard answers to shareholdersBoard represents policyholders

Stock companies are owned by shareholders, with a primary goal of generating profits for investors. Many large insurers operate this way.

Mutual companies are owned by the policyholders themselves. Profits are often returned to policyholders through dividends or lower premiums, leading to a focus on long-term customer satisfaction.

Financial strength ratings are critical when choosing an insurer. Independent agencies like A.M. Best rate each company's ability to pay claims. An A+ (Superior) rating indicates excellent financial health and a strong track record. Insurance is a promise of future protection, so you need to be certain your insurer will be financially strong when you need them.

At Bay Harbour Insurance Agency, we partner with a carefully selected group of financially strong company insurers. Our independence allows us to match you with the best fit for your needs, whether you're protecting your family or your business. For comprehensive business protection, explore our business insurance services.

Your Financial Safety Net: Key Insurance Products and the Claims Process

Insurance is your financial safety net, keeping unexpected events from becoming financial disasters. Understanding how different products work together is key to smart financial planning and business risk management.

For Long Island families and businesses, several products are essential. Auto insurance is required in New York State, but good coverage goes beyond legal minimums to protect your vehicle, cover medical bills, and shield you from liability. You can learn more about Auto Insurance New York State requirements to make informed choices.

Your home is a major investment, making homeowners insurance crucial. It protects the structure, your belongings, and provides liability coverage. Our guide to Homeowners Insurance Basics breaks down what every homeowner should know.

Life insurance is about protecting the people you love, ensuring your family can maintain their lifestyle and cover future expenses if you are no longer there to provide for them.

For businesses, Directors & Officers insurance protects company leadership from personal liability. Even small businesses can benefit from this coverage, as explained in our Directors & Officers Insurance Basics guide.

The Claims Process for Company Insurers

An insurer's true value is revealed during the claims process. Understanding the steps can reduce stress during a difficult time.

- Reporting: After ensuring everyone's safety, report your claim promptly. Most company insurers offer 24/7 reporting online, through mobile apps, or by phone. Provide accurate details about what happened.

- Investigation: A claims adjuster will be assigned to understand the incident and determine if the loss is covered by your policy. They may review reports, speak with witnesses, or inspect damage.

- Adjustment: The adjuster calculates the settlement amount based on your policy terms, coverage limits, and deductible.

- Settlement: The company insurer issues payment to you, a repair shop, or another involved party.

As a policyholder, it's important to provide honest information and cooperate with the investigation. Understanding key policy terms, like the difference between insureds and named insureds, can also be helpful. Our article on Insureds vs. Named Insureds: What's the Difference? explains these distinctions. A smooth, fair claims process is a hallmark of the best company insurers.

The Evolving Landscape: Technology and Future Trends

The insurance industry has transformed from a paper-heavy business into a tech-savvy sector, making coverage more accessible and personalized. Company insurers are rapidly embracing innovation.

Insurtech, the fusion of insurance and technology, is driving this change. Artificial intelligence is revolutionizing underwriting by analyzing vast datasets to create more accurate risk profiles, leading to faster approvals and more precise pricing.

Telematics and usage-based insurance are game-changers for safe drivers. Smart devices track actual driving habits, allowing for potential premium savings based on safe behavior.

Digital customer service has also skyrocketed. Policy management, which once required phone calls and paperwork, can now be handled from a smartphone. Paying bills, accessing ID cards, and updating information are simpler than ever.

Claims processing has also been streamlined. Policyholders can submit claims with photos from their phones, and some insurers use drones to assess property damage, speeding up the resolution process.

Technology also helps insurers tackle emerging risks. Twenty years ago, cyber threats were not a major concern for most businesses. Today, understanding the Risks Without Cyber Insurance is crucial. Similarly, business travel risks are constantly evolving, requiring adaptive insurance solutions to address new global challenges.

At Bay Harbour Insurance Agency, we accept how technology makes insurance more efficient. However, we believe there is still immense value in human expertise. We blend cutting-edge tools for convenience with the personalized guidance you need when it matters most.

Frequently Asked Questions about Company Insurers

Here are answers to some of the most common questions we hear from our Long Island clients about company insurers.

How do I choose the right insurance company?

Choosing the right company insurer means finding a reliable partner for your financial protection. Your specific needs should always drive the choice. Here are key steps to follow:

- Assess your needs: Determine what you need to protect, whether it's a new home, a small business, or both.

- Compare options: An independent agency can compare quotes and coverage from multiple top-rated company insurers to find the best value. The cheapest policy isn't always the best.

- Check financial strength: Look for insurers with an A+ (Superior) rating from A.M. Best. This rating indicates they have the financial stability to pay claims, even during widespread events.

- Research service: Investigate the insurer's reputation for customer service and claims handling. Look for 24/7 claims support and positive reviews.

An independent agency offers a significant advantage by providing unbiased advice. Learn more about the 10 Reasons to Choose an Insurance Agency Near You.

What's the difference between an insurance agent and an insurance company?

The insurance company (or carrier) is the entity that underwrites your policy, assumes the financial risk, and pays claims.

An insurance agent is your licensed guide and advocate. We help you steer policies, understand coverage, and select the right plan.

- Captive agents work for a single insurance company.

- Independent agents, like us, represent multiple company insurers, allowing us to shop the market to find the best fit for you.

How can I save money on my insurance premiums?

There are several smart ways to lower your insurance costs without sacrificing crucial coverage.

- Bundle your policies: Most company insurers offer significant discounts for combining policies like auto and home.

- Raise your deductible: A higher deductible (the amount you pay before insurance kicks in) can lower your premium. Ensure you can comfortably afford the deductible amount.

- Shop around regularly: As your life changes, so do your insurance needs. An independent agent can easily re-shop your policies to ensure you're getting the best rates.

- Ask for discounts: Insurers offer various discounts for safe driving, home security systems, and more. We can help you identify all the discounts you qualify for.

For more local tips, check out our guide on How to Save Money on Home Insurance in NY.

Conclusion: Partnering with the Right Experts for Your Protection

Understanding company insurers is the first step toward making smart decisions about your financial security. You now know how insurers assess risk, the different types of coverage available, and why an insurer's financial strength is so important.

We've seen how technology is making insurance more convenient, while also creating new risks that require modern solutions. While this knowledge is powerful, applying it to your unique situation is where expert guidance becomes invaluable. Every Long Island family and business has different needs, and a one-size-fits-all policy rarely provides the best protection.

This is where the independent agency advantage comes in. We represent multiple top-rated company insurers, allowing us to shop the market and find the coverage that truly matches your needs and budget. Our client-centered service begins with listening to you. Whether you're in Patchogue, Medford, or Sayville, we take the time to understand your situation before recommending a plan.

We know Long Island, from its unique coastal risks to New York's specific insurance requirements. This local knowledge, combined with our access to a wide range of company insurers, ensures you get personalized service and comprehensive options.

Ready to build a protection plan that gives you true peace of mind? We're here to simplify the complex world of insurance. Contact our Patchogue, NY personal insurance agency for a personalized quote today.